I did personality test for investor - what type am I?

Where can you find personality test for investors?

I did my test on Marketpsych.com - link below:

http://tests.marketpsych.com/test_question.php?id=8

Test consists of 74 questions and takes abiut 20 minutes.

What was my result?

I copied my report and pasted it below.

1) Personality factors:

ConscientiousnessConscientiousness Factor: Your result is High.

- Conscientiousness describes your relative ability to plan and organize towards achieving goals and to exercise self-control.

- You scored in the HIGH range for conscientiousness. Intelligent activity involves contemplation of long-range goals, organizing and planning routes to these goals, and persisting toward one's goals in the face of short-lived impulses to the contrary. You can achieve high levels of success through purposeful planning and persistence. You are likely to be positively regarded by others as intelligent and reliable. On the down side, some people may see you as rigid or perfectionistic. EmotionalityEmotionality Factor: Your result is Very Low.

- Emotionality is characterized by stress-sensitivity and more frequent experiences of negative emotions than others.

- You scored in the LOW range on emotionality. You are relatively more calm, emotionally stable, and free from persistent negative feelings when compared to high scorers. Freedom from negative feelings does not mean that you experience more positive feelings. You may be reckless in dangerous situations and take more risks than others (sometimes without knowing that you are doing so). In general you are probably secure, hardy, and relaxed even under stressful conditions. ExtraversionExtraversion Factor: Your result is Below Average.

- Extraversion is characterized by a desire to socialize and a tendency to optimism. Extraverts derive energy from interactions with others, while introverts' interests are fueled by introspection.

- You scored in the NEAR AVERAGE range on extraversion. You are moderate in activity and enthusiasm. You enjoy the company of others but you also value privacy. OpennessOpenness Factor: Your result is Very High.

- Openness to new experiences describes a willingness to experiment with tradition, to seek out new experiences, and to think broadly and abstractly.

- You scored in the HIGH range on openness. You are intellectually curious and tend to be, compared to closed people, more aware of your feelings. You probably tend to think and act in individualistic and nonconforming ways. Open and closed styles of thinking are useful in different environments. An open intellectual style may serve you well as a psychologist, professor or investor. Research has shown that closed thinking is related to superior job performance in police work, sales, service occupations, and short-term trading. AgreeablenessAgreeableness Factor: Your result is Below Average.

- Agreeableness reflects a concern with cooperation and social harmony.

- You scored in the NEAR AVERAGE range on agreeableness. You are likely to balance a healthy skepticism about others' motives with a desire to cooperate and get along. You are willing to extend yourself for others and compromise, but you may prefer that they first demonstrate good will.

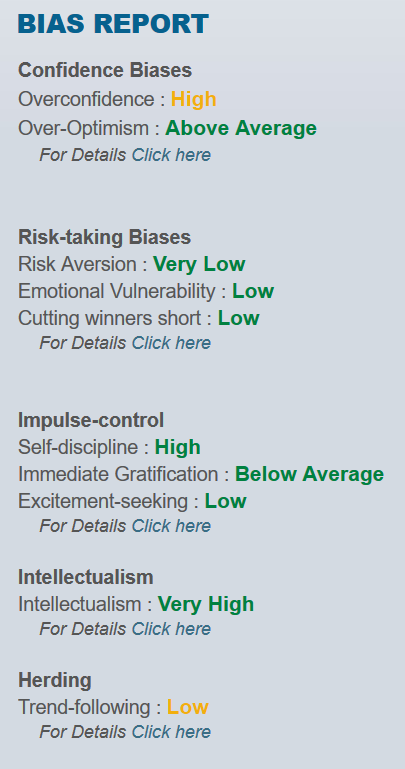

2) Bias report

Confidence-Related BiasesOverconfidence: Your result is High.

- "Mutual fund managers, analysts, and business executives at a conference were asked to write down how much money they would have at retirement and how much the average person in the room would have. The average figures were $5 million and $2.6 million, respectively. The professor who asked the question said that, regardless of the audience, the ratio is always approximately 2:1."

- ~ Whitney Tilson (Fool.com)

- Overconfidence refers to the tendency to see oneself and one's abilities as better than they actually are. Specifically, overconfident investors misinterpret the accuracy and importance of their information (what they know) and overestimate their skill in analyzing it. Additionally, overconfidence results in a tendency to underestimate investment risk and to have higher turnover.

- Men are more likely to be overconfident than women, and young adults are more likely to be overconfident than older adults. Ironically, "experts" are more overconfident than lay-people, as they often overweigh the predictive power of their own models. Additionally, more difficult decisions (e.g. forecasting the market) inspire more overconfidence in forecasters.

- "Who has confidence in himself will gain the confidence of others."

- ~ Leib Lazarow

- Overconfidence can be destructive in investing, where a belief in one's superiority does not translate into bigger profits. However, overconfident financial planners have been found to attract more business than less-confident rivals, even while having lower overall performance than their colleagues. In many business endeavors, overconfidence both attracts more clients and leads to greater overall risk-taking. However, in investing, overconfidence can lead to long-term underperformance if it is not balanced by experience. HIGH SCORERS:"Before you attempt to beat the odds, be sure you could survive the odds beating you." ~ Larry Kersten (author and sociologist)If you are a high scorer, to balance your potential for overconfidence in investing, you should:

- Practice humility. No matter how well you have been investing, you can suffer losses if you approach the markets with arrogance about past profits or entitlement to new ones. Every day consider the possible market risks, and actively seek out new ones.

- Think before you leap. If you have a problem acting too quickly on your private information, then deliberately pause for a brief cooling-off period between having a strong opinion about the market and executing it. Remember, there will always be more opportunities.

- After a string of wins, be careful of feeling that you're invincible. It's usual, after a series of wins, to feel "on top of the world." However, beware of taking on excessive risk or leverage at these times. Overconfident hubris is the result of a string of wins, and it nearly always leads to big losses.

- Engage in a more thorough evaluation of your investment plans. In particular, remember to look at historical parallels and to perform adequate historical analysis of your investment ideas.

Optimism: Your result is Above Average.

- "For myself I am an optimist - it does not seem to be much use being anything else."

- ~ Sir Winston Churchill, 1954.

- Optimism refers to the rose-colored lenses through which high-scorers view the world. Optimism is associated with "confidence" biases because many people who are overly optimistic overestimate their chances of success (as in overconfidence). Yet optimistic people do not typically take excessive risks. They are likely to take calculated, moderate risks. In fact, optimistic people would not want to risk losing a sum of money large enough to depress their mood.

- Optimistic people often avoid negative information and seek out evidence confirming their positive outlook. This search for positive confirmation is a type of denial, On the flip-side of optimism is pessimism, which characterizes low-scorers.

- As with the other confidence "biases," optimism benefits businesspeople, politicians, and other professionals whose ability to attract business often depends on their attitude. However, in the financial markets, excessive optimism can lead to superficial analysis and denial of important, negative evidence. One potential result of over-optimism is not saving adequately for retirement. One financial planner said: "It's the ornery, suspicious people who save the most for retirement. The happy ones just figure everything will be okay, and when they near retirement, they come to me, and I have to help them ratchet down their expectations."

- The optimistic investor may find himself holding excessive risk in his portfolio while denying evidence of growing dangers. Many optimistic investors who believed in the "New Economy" and the outstanding growth potential of internet stocks found themselves over-exposed to the volatile technology sector in late 2000 and 2001. It was common to hear over-optimistic pundits urging investors to "stay the course" (or "dollar-cost average") in their technology stock investments in late 2000 and 2001.

- Optimistic people tend to be resilient. Additionally, optimistic people often believe that "everything is going to work out for the best," which fosters energetic activity and success in many areas of life.

- "For myself I am an optimist - it does not seem to be much use being anything else."

- ~ Sir Winston Churchill, 1954. HIGH SCORERS:If you are a high scorer, you are optimistic. You tend to see the glass as "half-full," and you generally see a positive future ahead for you and the world. Your optimism is, in general, a great gift. However, in your investing, you should be careful:

- Don't believe the hype. You are more susceptible to believing a good story. Remember, a good company does not make a good stock. Only invest when you can look through the buzz at the underlying fundamental data.

- Most investors stop paying attention to risks when things are going well. Because of your higher level of optimism, you are more susceptible to ignoring investment risks during winning streaks than others. Be sure to seriously investigate the potential risks of your investments as often as appropriate.

- Budget extra money. Save more than you think you'll need for business projects and retirement. You're likely to underestimate the money you'll need in retirement, and medical studies show that you're likely to live longer than pessimists.

Risk-Related BiasesLoss Aversion:

- Stephen W. Boesel was the director of the $11 billion T. Rowe Price Capital Appreciation Fund until mid-2006. The fund has a 16 year winning streak (as of mid-2007), and it is the only equity fund to report 16 positive years in a row. Boesel summarized his money management strategy for the fund in the Wall Street Journal as follows: "We win by not losing." Notice that Boesel doesn't try to find winners, rather, he avoids losers. In order to "not lose," the fund cuts its losers short (and lets its winners run).

- "Cut your losers short" is a Wall Street aphorism that encourages investors to do the opposite of an innate tendency. Most investors are inclined to hold losing positions too long. This is the single most common and costly mistake investors make.

- Most amateur investors either avoid thinking about losing positions or they hope for a "comeback" so they can exit the investment at "break-even." Ironically, if an investor is bailed out by the market, they tend not to learn from their mistake, leaving them more vulnerable to later losses.

- Most "Rogue Traders," including Nick Leeson (Barings) and Toshihide Iguchi (Daiwa Bank), who both lost over $1 billion, ended up with huge losses because they could not muster the courage to bail out of losing positions in the beginning, and then they developed illegal strategies for hiding their snowballing losses.

- One of the three tenets of the 2002 Nobel-prize winning theory of economic decision-making called "prospect theory" is that people avoid taking losses, even when that avoidance will likely lead to larger losses later. For example, when faced with the choice between (1) losing a definite amount of money, or (2) gambling on a "come-back," most people prefer to take the gamble. Note that most people will choose the gamble even when the expected value of the gamble is more than twice as severe as the definite loss.

- "Even being right 3 or 4 times out of 10 should yield a person a fortune if he has the sense to cut his losses quickly on the ventures where he has been wrong."

- ~Bernard Baruch, Financier

- After experiencing a recent loss, most investors will become more loss averse. Losses of any kind have this effect - the death of a loved one, divorce, illnesses, accidents, work-related losses, and financial losses - all increase this propensity.

- Most people suffer from loss aversion, though it is stronger in high scorers than in low scorers. HIGH SCORERS:The result of loss aversion is "throwing good money after bad." If you are a high scorer, you are more likely to hold onto losing investments for longer than originally planned. The following recommendations assume that you are an active investor:

- Ask yourself, "All things being equal, would I enter this position today?" If your answer is "no," then place it on your sell list.

- When in a losing position, beware of thinking, "I'll just wait and see what happens." Notice any rationalizations or excuses you make in order to hold a losing position longer.

- If you already have a track record of holding losers too long, and you have little experience, beware of purchasing naked options and shorting.

- 4. If you have the technology, keep track of your Win/Loss size ratio. Investors can discover if they are holding losing investments too long by keeping track of the size of their winning and losing investments. The ratio should be more than 1 (more money in open winners than open losers). One can also monitor the length of time they hold your losing versus winning investments to diagnose this problem.

Emotional Vulnerability: Your result is Low.

- "Success in investing doesn't correlate with I.Q. once you're above the level of 25. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.

- ~ Warren Buffett

- The Buffett quote above indicates that the ability to manage your impulses, particularly those stemming from emotion, leads to greater investment success than intelligence alone.

- If you are a high scorer on emotional vulnerability, you are likely to experience panic, confusion, and helplessness when under pressure or experiencing stress. If you are a low scorer, you feel more poised, confident, and clear-thinking during stressful times.

- "We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful."

- ~ Warren Buffett

- Buffet can maintain a long-term perspective during emotional periods in the markets. As a result, he can go against the prevailing market sentiment (and thus take advantage of mis-pricings). Such emotional stability is essential in order to find bargains during periods of market volatility. LOW SCORERS:

- 1. You are probably more calm than most during market volatility. Nonetheless, become aware of the triggers for negative emotional states during investing. If emotions are a problem for you, then see the recommendations above and consider whether you can adapt your investing style to accommodate.

Risk Aversion

Loss Aversion: Your result is Very Low."You get recessions, you have stock market declines. If you don't understand that's going to happen, then you're not ready, you won't do well in the markets."~ Peter Lynch

- Risk aversion refers to an excessive fear of risk-taking. Risk aversion can trigger investor hesitation, indecision, and "analysis paralysis." Many investors with high risk aversion experience difficulty "pulling the trigger" in volatile markets.

- Some investors experience risk aversion as "waiting for confirmation." Unfortunately, waiting for expected price movement erodes profits. Indulging the inclination to delay can precede impulsive entries and exits later on.

- When investing without adequate due diligence, risk aversion is appropriate. Investors should do background research to gain confidence. Sometimes losses are due to random events, and in those cases it is helpful to understand the laws of probability and the inevitability of draw-downs (an understanding derived from having a solid investment philosophy). HIGH SCORERS

- High risk aversion can be managed in several ways. Amateur investors who have high risk aversion should probably entrust their money to a trusted professional (such as a financial advisor). Most advisors will take an appropriate amount of risk for the long-term growth of your portfolio, and high scorers will not have to worry about the best course of action to take with their assets.

- As with many of the volatility-sensitive profiles above, risk averse investors should check the value of their portfolios as infrequently as possible.

- Confidence can be built with market experience, gradual exposure to market risk, education, and the constructive challenging of one's fears. LOW SCORERS:

- Very Low scorers should beware of taking excessive risk. But in combination with adequate self-discipline, education, historical knowledge, experience, and preparation, a low score on risk aversion is usually beneficial for investors. Cutting Winners Short: Your result is Low.

"Selling companies that are doing well and purchasing ones that are faring poorly is like watering the weeds and cutting the flowers."~ Peter Lynch, Fidelity Investments"Our favorite holding period is forever."~ Warren Buffett

- J.R. Simplot is an 8th grade drop-out and a self-made multi-billionaire. He made his fortune through saavy investments in potato farming and french fry production. Currently he owns the largest ranch in the United States, the ZX Ranch in southern Oregon. His ranch is larger than the state of Delaware. Despite his tremendous wealth, Simplot is a modest man. He describes his accumulation of wealth to Eric Schlosser (author of Fast Food Nation):

- "Hell, fellow, I'm just an old farmer got some luck," Simplot said, when I asked about the keys to his success. "The only thing I did smart, and just remember this - ninety-nine percent of people would have sold out when they got their first twenty-five or thirty million. I didn't sell out. I just hung on." [bold added]

- In general, most people sell their winning investments too soon ("cutting winners short"). According to some experts, selling winning investments too soon is a result of "seeking pride." Others believe that cutting winners short is related to obsessiveness. The truth is a mix of both. Everyone is susceptible to this bias to some extent.

- If you are a HIGH SCORER or are guilty of cutting your winners short, you should:

- When you feel yourself becoming worried about a winning position, don't impulsively sell. Instead re-evaluate your selling criteria. Did the investment meet your profit target? Has something fundamental changed about the security that indicates you should sell now?

- Be prepared for your short-term winners to give back some of their gains. Reversals are very common after a rapid, large price rise, especially when it is unsupported by news.

Discipline and PlanningSelf-Discipline: Your result is High.

"One trait that was shared by all the traders is discipline."~ From "Wizard Lessons", Stock Market Wizards

- Self-discipline is what many people call will-power. Self-discipline refers to one's ability to persist at difficult or unpleasant tasks until they are completed. People who possess high self-discipline are able to overcome their reluctance to begin tasks and can stay on track despite distractions.

- Low scorers are more likely to procrastinate and show poor follow-through on their plans. Impulsive trading, erratic performance monitoring and ignoring investment positions for long periods are all characteristic of traders with very low scores.

- In a survey of 200 currency traders in continental Europe, self-discipline was rated the second most important factor in trader success. (The most important factor was quick reaction time). In a study of the psychological factors correlated with financial success, "self-control" (a close relative of discipline) was the most significant factor.

- Self-discipline supports many of the habits that together contribute to success. One of those habits is the ability to meticulously analyze one's performance. What factors led to a successful business decision? What happened to cause an unanticipated loss? Self-discipline is necessary for collecting and organizing this information.

- Disorganized investors can often compensate for low self-discipline by hiring disciplined professionals to work with, or for, them.

Immediate Gratification: Your result is Below Average.

""Business opportunities are like buses, there's always another one coming."~ Richard Branson

- "Immediate gratification" is the preference for small, immediate rewards over larger, more distant rewards. People who "eat dessert first" are giving in to immediate gratification urges. Impatience and impulsiveness are characteristic of high-scorers.

- Greed is a close cousin of excitement-seeking. Greed is often described as "excessive desire" for money or valuables. Anyone who has experienced the feeling of greed can relate to that pressured, desperate need to get more money NOW. People who are high in immediate gratification are more likely to engage in gambling behavior (taking inappropriate risks), and they are more likely to experience a greedy state of mind when evaluating potential investments.

- Bill Miller, Chairman of Legg Mason Capital Management, beat the S&P 500 index every year for 15 consecutive years (from 1991-2005). When interviewed by the Wall Street Journal in January 2005, "Bill Miller Dishes on His Streak and His Strategies," he attributed his success to a very simple concept: "The biggest opportunity for investors is really thinking out longer term... So we tried to adjust the construction of our portfolio to reflect the neglect that analysts and portfolio managers have given to those factors. Our turnover rate has dropped significantly as we've tried to lengthen our time horizon."

- Investors who score highly here should try to perform adequate up-front research and cultivate patience when investing.

- HIGH SCORERS may find the following helpful:

- 1. Remember Bill Miller and Richard Branson's quotes above. Patience is a cardinal virtue of investors. Another "perfect" stock or setup will always come along. It is financially unhealthy to chase performance.

- 2. As Bill Miller describes, widen your time-perspective. This is especially useful when feeling a need to perform. Looking ahead at farther horizons or larger-scale charts can diminish your urge to make impulsive decisions now.

Excitement-Seeking: Your result is Low.

"The individual investor should act consistently as an investor and not as a speculator. This means... that he should be able to justify every purchase he makes and each price he pays by impersonal, objective reasoning that satisfies him that he is getting more than his money's worth for his purchase."~ Benjamin Graham

- Excitement-seeking describes the tendency to pursue emotionally arousing activities. Excitement-seeking is seen in investors who make large bets more for the thrill of the gain than an understanding of the game. Note that prudent, calculated excitement-seeking is seen in most successful investors.

- The difference between successful and unsuccessful excitement-seekers is that the successful ones are more excited by a good decision than a large financial outcome. They realize that excellent research, organization, management, and execution lead to profit. They value the game more than the material rewards that will accrue from playing it well.

- Richard Branson, the Billionaire British entrepreneur, is well known for his adrenaline-raising antics to promote his various businesses. He argues that fun is necessary to his work:

- "A business has to be involving, it has to be fun, and it has to exercise your creative instincts."

- ~ Richard Branson

- A problem arises when your investing is all about fun, with profits only secondary. It is important that you enjoy investing, but it is also crucial that you not invest purely for the sake of that enjoyment. Rather, you ought to enjoy making profits as a result of following your investment plan.

IntellectualismIntellectualism: Your result is Very High.

"An intellectual is a man who takes more words than necessary to tell more than he knows."Dwight D. Eisenhower (1890 - 1969)

- Intellectual investors enjoy investigating complex concepts and abstractions. In general, intellectualism is a good thing for investors. High intellect underlies one's curiosity about new investment ideas, and most great investors are intellectual.

- However, without a disciplined and experienced mind, high intellectualism may lead to gathering "too much information" and "over-thinking." A hallmark of the excessively intellectual investor is the use of unnecessarily complex assumptions and methodologies.

- Psychological research demonstrates that gathering more than 3 pieces of relevant information about any one decision leads to deteriorating decision quality. Apparently, analyzing too many independent details leads to eroded profitability.

- Investors who are low scorers on intellectualism can more easily remain focused and without distractions or tangents in their thinking, but they are less sensitive to new ideas and opportunities. In contrast to investors, many successful traders score below average on intellectualism.

- "Very low" scorers may not feel curiosity about new business ideas, which can reduce their performance if market conditions change. HIGH SCORERS:"Nothing contributes so much to tranquilizing the mind as a steady purpose - a point on which the soul may fix its intellectual eye."Mary Wollstonecraft Shelley (1797 - 1851)

- Highly intellectual investors may have trouble with mind wandering. Their endless curiosity about new business concepts or models may hamper the disciplined management of their investments.

- Notice if you are "missing the forest for the trees." Successful business doesn't have to be difficult or complicated. Many people consistently profit with businesses that appear simple, but which are based on tried-and-true principles.

HerdingTrend-Following: Your result is Low.

"Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one."~ Charles MacKay (1841) Extraordinary Popular Delusions And The Madness Of Crowds

- Trend-following refers to one's tendency to follow the crowd, relying on others for leadership and critical thinking. Trend-following can be profitable for investors (though many contrarians would disagree), provided that they recognize signs of trend formation and dissipation. Momentum investors are an example of trend-followers.

- "Never, Ever Listen to Other Opinions.

- To succeed in the markets, it is essential to make your own decisions. Numerous traders cited listening to others as their worst blunder. Walton and Minervini lost their entire investment stake because of this misjudgement."

- ~ Jack Schwager, Stock Market Wizards, Wizard Lessons #29

- Contrarians score low on trend-following. Contrarians tend to bet against current trends or opinion when they are identifiably incorrect. Contrarians typically view the market consensus with suspicion, and are sometimes described in the same sentence as value investors.

- Because the many market opportunities are created by the misbehavior of the mass of investors, an understanding of crowd psychology is useful for investors.

- "If your mind is not in gear with the markets, or if you ignore changes in mass psychology of crowds, then you have no chance of making money trading." ~ Alexander Elder (1993) Trading for a Living LOW SCORERS:

- You have the innate advantage of searching for opportunities away from the crowd. Investing in overlooked markets or sectors may fit your personality. Low scorers are often value investors.

- Beware of betting against powerfully trending markets. Fading trends may be appealing to low scorers, but doing it well requires patience, vigilance, and knowledge of the signs of market reversals. Timing is key.

I left the descriptions for only my results in purpose to motivate you to do the test yourself 😀

My conclusion:

I am happy about results of my test in general, nevertheless I know what my major weaknesses are and I will strive for improvement.

I recommend you to do this test if you investor or you want to be one.

I would have to work on humility because it turned out that I am overconfident and very optimistic person. After a streak of wins I wolud have to definitely relax and stay away from making decisions for a while.

What I was expecting I had a problem with following the herd but I was quite surprise, that this test treated this as negative. Perhaps the authors made this test rather for traders and speculants, that play trend-following type of game and always say "trend is your friend". I often look for the end of some speculative bubbles too early, like bitcoin last year. Unfortunately I started to ring the alarm bell way too early and lots of cryptocurrency investors made a good laugh at me for months. Luckily it was me, who had the last laugh 😀 But still, I have to work to be more herd-friendly and not rebel against such a strong trends in the future, letting them achieve absolute schizphrenic mania first.

Best investing regards!

Albert "Longterm" Rokicki

Email: kontakt@longterm.pl

Kanał Youtube: www.youtube.com/user/alrokas

Fanpage na Facebooku: www.facebook.com/longtermblog

Twitter: https://twitter.com/Longterm44